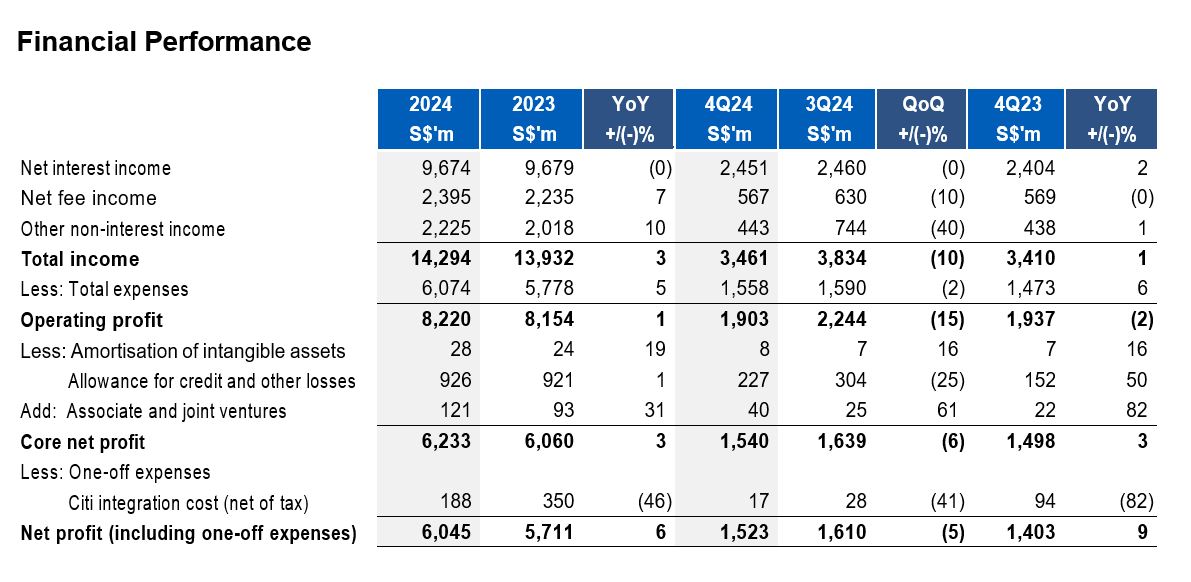

UOB Group reported a record net profit of S$6.0 billion, up 6%, for the financial year ended 31 December 2024 (FY24).

The Board recommends the payment of a final dividend of 92 cents per ordinary share. Together with the interim dividend of 88 cents per ordinary share, the total dividend for FY24 will be S$1.80 per ordinary share, representing a payout ratio of approximately 50%.

As part of the Bank’s capital distribution strategy, the Board announced a S$3 billion package to distribute surplus capital over the next three years. The package comprises special dividends and share buybacks. A special dividend of 50 cents per ordinary share is recommended in 2025, distributing S$0.8 billion of UOB’s surplus capital. This is also to mark the Bank’s 90th anniversary. In addition, a new share buyback programme of S$2 billion has been introduced.

In FY24, the Group’s net profit grew 6% from a year ago to a record S$6.0 billion, driven by strong net fee income and trading and investment income. Net interest income remained steady at S$9.7 billion as a healthy loan growth of 5% was moderated by the effects of interest rate movements on our net interest margin. Net fee income grew 7% to S$2.4 billion, led by a double-digit growth in wealth fees, stronger credit card fees and higher loan-related fees. Asset quality remained stable with non-performing loan (NPL) ratio at 1.5%.

Group Wholesale Banking continued to see strong momentum in its overall performance. Trade loans increased 20% from the year before. Transaction banking business demonstrated consistent growth, and now accounts for more than half of the Group Wholesale Banking income. Cross-border income also grew, and now makes up more than a quarter of the Group Wholesale Banking income.

Group Retail also performed well in FY24. Credit card fees remained strong, growing 18% year on year, backed by continued consumer spending and an enlarged regional franchise. Wealth management income rose 30%, supported by improved investor sentiments. The Group continued to see strong net new money inflows, bringing high-net-worth assets under management to S$190 billion, a 8% year-on-year growth. Organically, the Group added more than 850,000 new-to-bank customers in FY24, of which around half were acquired digitally. As at end of 2024, our retail customer base in Southeast Asia has expanded to nearly 8.4 million.

The Group continued to drive the sustainability agenda in 2024. In November 2024, we issued our second progress report on our net-zero commitment and are making good progress across all priority sectors, especially in the power sector. As at end of December 2024, the Group’s sustainable financing portfolio increased 43% to S$58 billion. The Group remains committed to supporting our customers on their green journeys.

CEO Statement

Mr Wee Ee Cheong, UOB’s Deputy Chairman and Chief Executive Officer, said, “The Group achieved a record net profit in 2024, driven by strong fee income as well as robust trading and investment income. Our long-term investments in regional platforms and capabilities are paying off, and we expect continued revenue growth this year.

“Despite global uncertainties, we are confident that the ASEAN region will remain resilient, supported by higher domestic retail spending and stronger influx of foreign direct investment. Our strengthened market position in our key ASEAN markets, enlarged customer base and enhanced platforms will position us well to seize regional opportunities amid a reconfiguration of global trade and supply chains.

“In 2024, we completed the integration of our Citigroup portfolio in Thailand, following successful integrations in Malaysia and Indonesia in 2023. Integration for Vietnam is on track to be completed by this year. We will continue to harness cross-sell synergies, manage costs, and enhance our products and solutions to better serve our expanded customer base.

“This year marks UOB’s 90th anniversary. We have come so far thanks to the unwavering support of our stakeholders, partners, and customers. We will continue our disciplined approach to pursuing long-term growth with stability, ensuring we bring greater value to everyone we serve.”

FY24 versus FY23

Net profit for FY24 grew 6% to a record S$6.0 billion from a year ago, boosted by strong net fee income and trading and investment income. Excluding the one-off expenses, core net profit was at S$6.2 billion.

Net interest income was stable at S$9.7 billion as healthy loan growth of 5% offset the effect of net interest margin contraction from interest rate movements.

Net fee income grew 7% year-on-year to S$2.4 billion, led by double digit growth in wealth management fees from improved investor sentiments, alongside stronger card fees on an enlarged regional franchise, and higher loan fees as lending and capital market activities picked up.

Other non-interest income rose 10% to S$2.2 billion, driven by robust customer-related treasury income from increased retail bond sales and strong hedging demands, as well as good performance from trading and liquidity management activities.

Excluding one-off expenses, core operating expenses increased 5% to S$6.1 billion as the Group continued to invest in building regional capabilities. Total allowance was relatively stable at S$926 million with total credit costs on loans at 27 basis points.

4Q24 versus 3Q24

Net profit for the fourth quarter was 5% lower at S$1.5 billion. Net profit excluding one-off expenses was also at $1.5 billion, as Citi integration costs tapered off.

Net interest income held steady at S$2.5 billion. Net interest margin narrowed to 2.00% on lower benchmark rates offset by loan growth of 1%. Net fee income eased from last quarter’s high to S$567 million due to the seasonal slowdown in loan-related and wealth activities. Other non-interest income normalised to S$443 million, after an exceptional 3Q24 that benefitted from market volatilities.

Total core operating expenses declined 2% to S$1.6 billion with the cost-to-income ratio at 45.0%. Total allowance decreased to S$227 million, mainly due to write-back of general allowance previously set aside. Total credit costs on loans was at 25 basis points for this quarter.

4Q24 versus 4Q23

Net interest income was up 2%, supported by loan growth of 5% while net fee income and other non-interest income were relatively unchanged at S$567 million and S$443 million respectively.

Core operating expenses increased from investment in franchise growth, with core cost-to- income ratio at 45.0%. Total allowances increased to S$337 million on higher specific allowance.

Asset Quality

Asset quality remained resilient with NPL ratio at 1.5% as of 31 December 2024. The non- performing assets coverage stayed adequate at 91% or 194% after taking collateral into account.

Capital, Funding and Liquidity Positions

The Group’s capital position remained strong with Common Equity Tier 1 Capital Adequacy Ratio at 15.5% for the quarter. Liquidity remained healthy with this quarter’s average all- currency liquidity coverage ratio at 143% and net stable funding ratio at 116%, both well above regulatory requirements. Loan-to-deposit ratio was healthy at 82.7%.