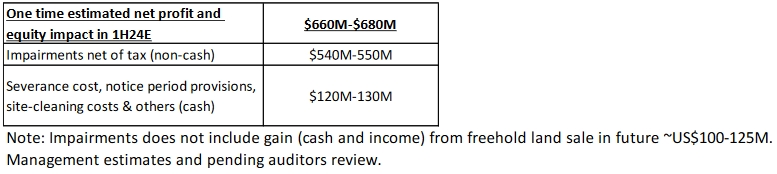

Indorama Ventures Public Company Limited (SET: IVL) has announced its mid-year strategic review of the progress on its IVL 2.0 plan with an announcement to divest two plants, including a PET/PTA site in the Netherlands and an Ethylene Oxide (EO) and derivatives facility in Australia. Together with optimizations of other sites, the company anticipates a total impairment and expense provision of $660-680 million in 2Q24, but will bring in about $300 million in cash proceeds.

IVL 2.0 was conceived as a response to structural shifts in the macroeconomic and industry landscape, primarily:

- Continued overcapacity in China—the majority of which is integrated—is changing the competitive dynamics of the polyester ecosystem.

- The advent of peak oil and electric vehicles in Western markets is resulting in reduced investment in new refinery production while the additional costs of carbon taxation requires significant additional capital expenditure. Therefore, the building of new refineries in Asia, where demand continues to grow for refinery products, represents a significant challenge to the cost structure of Western refineries.

- The company believes the U.S Federal Reserve intends to keep benchmark interest rates higher for longer in an environment of sustained inflation, jeopardizing economic growth

Regarding the IVL 2.0 vision, in the last six months the company has made pivotal organizational changes, reflecting a proactive approach to not only confront the current market challenges but to thrive on the new opportunities that the changes bring. The company’s CPET and Fibers segments have made good progress in transitioning to the next generation of home-grown talent, while Indovinya and the Packaging business (renamed Indovida) are progressing with their plans for upcoming public listings.

The company is broadening and deepening its leadership bench to drive the strategic initiatives under IVL 2.0. The below chart depicts the new dedicated corporate executive team, which is tasked with shaping the company’s story, driving alignment and synergies, and helping with governance around right sizing the company’s portfolios.

The four business segments have been reorganized with a lean management structure, and accountable and empowered leaders who take ownership of their respective businesses. The objectives are clearly mandated, and the delivery is on track to create industry-leading returns across cycles.

As a part of the asset optimization plan under IVL 2.0, the company has closed its PET/PTA site in the Netherlands, and an Ethylene Oxide (EO) and derivatives facility in Australia. Together with optimizations of other sites, it anticipates a total impairment and expense provision of $660-680 million in 2Q24.

The cash component will be paid in 2H24, expected to be compensated by working capital release of $110-130 million from closed sites. This does not include estimated cash gains of $100-125 million expected from the sale of freehold land, to be realized in due course. These actions represent a significant proportion of the company’ asset optimization program, and it does not expect material additional impairments arising from this program.

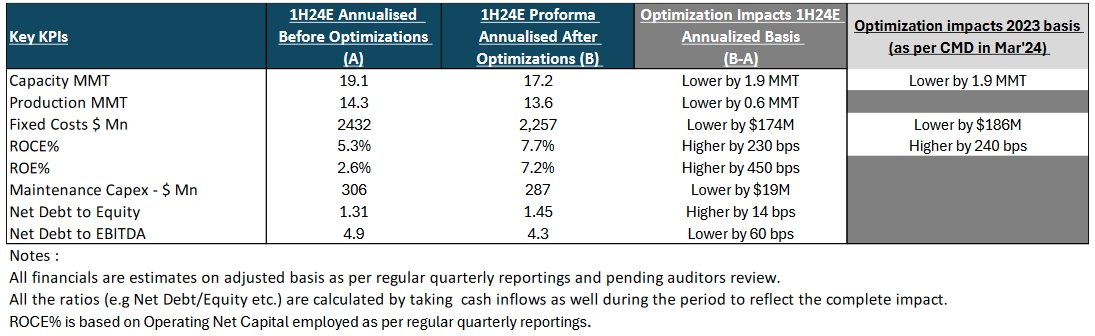

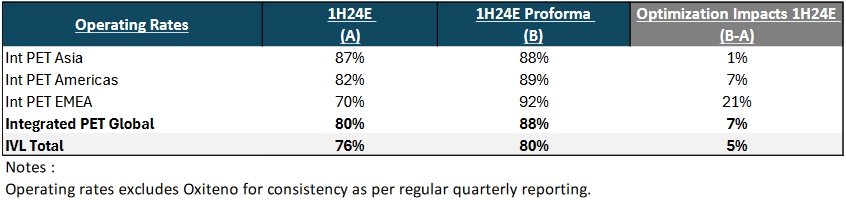

The below tables demonstrate the impact of these optimizations, showing proforma results based on an adjusted 1H24E performance. The actions primarily impact the integrated PET business, where operating rates improve by 7%. Revenue will remain largely unchanged as we continue to serve customers from other sites. By taking these actions, the company is strengthening its asset base and improving cash flow and quality of earnings to increase ROCE by ~230 basis points and ROE by ~450 basis points. With the full realization of savings, Net Debt/Equity will rise to about 1.5x, well within the debt covenants’ norms of 2.0x, while Net Debt/EBITDA reduces by ~60 basis points.

Amid challenging and volatile financial markets in the first half of 2024, the company has proactively managed its funding requirements through raising $1.3 billion for capex and investments to refinance debt maturities and additional liquidity. The funding has been executed for longer tenor at reduced spreads, and to diversify the company’s sources of long-term financing.

On 31 March 2024, the company had $2.5 billion liquidity in the form of cash, cash under management, and unutilized banking lines. Furthermore, in July 2024 the company successfully completed a THB 15 billion perpetual debentures offering, due to repay outstanding perpetual debentures of THB 15 billion on a first call date in November 2024. These successful transactions reflect financial institutions’ and investors’ confidence in the steps being taken to strengthen the company’s financial profile and favorable long-term business outlook.

According to the report by Reuters, IVL is expected to list Indovida in 2025 in Asia, while its IOD business ‘Indovinya’ is expected to be listed in 2026 in Western markets.