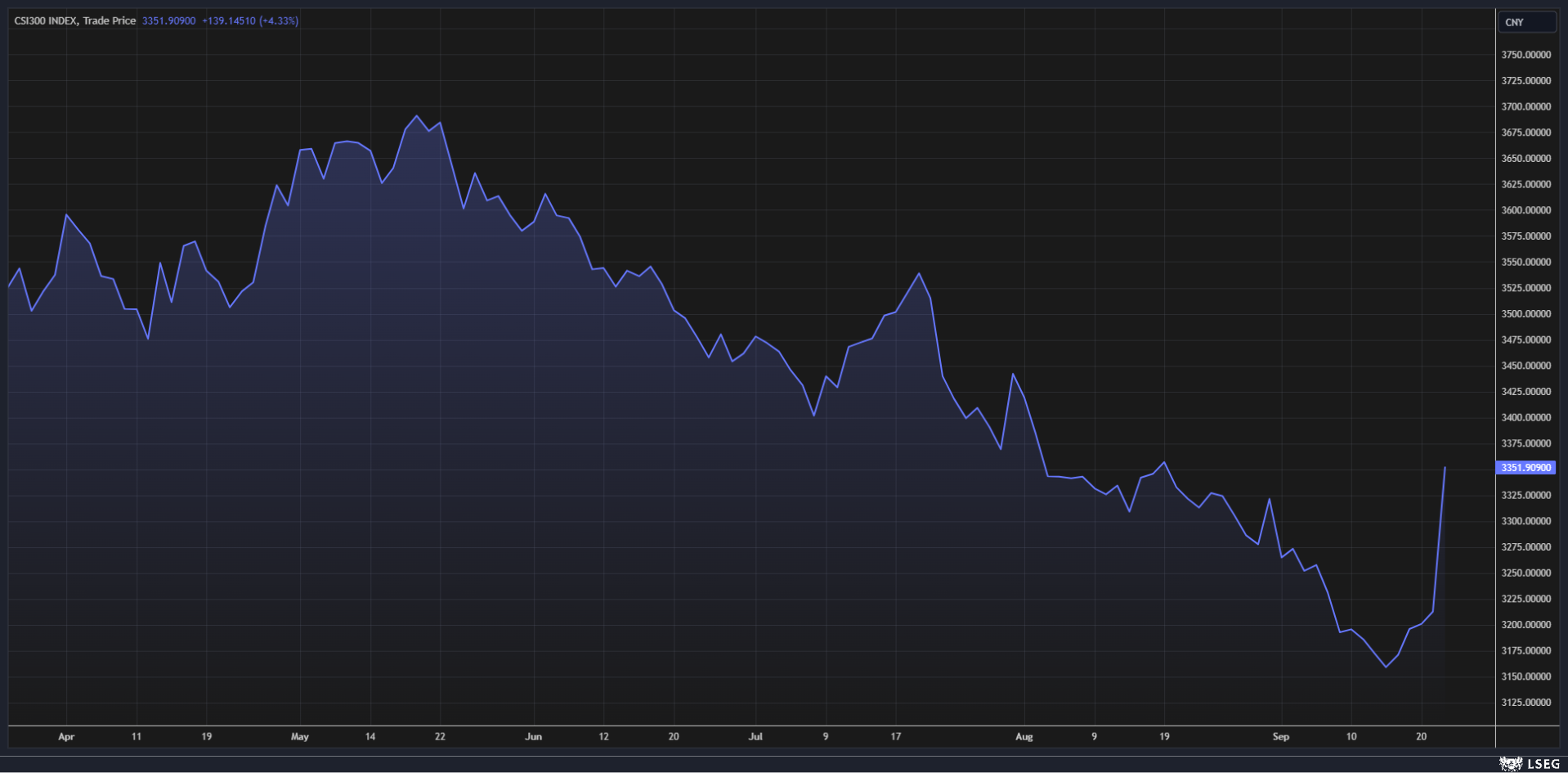

Mainland China’s CSI 300 saw its most significant surge in over four years on Tuesday following the announcement of various policy relaxations during a rare briefing by central bank governor Pan Gongsheng.

The index climbed by 4.33%, marking its most profitable day since July 2020, to conclude at 3,351.9. After the decision, Hong Kong’s Hang Seng index also notched a 4.13% gain.

The People’s Bank of China (PBOC) plans to decrease the reserve requirement ratio for banks by 50 basis points without specifying a precise timeline. Additionally, it disclosed a reduction in the seven-day reverse repurchase rate from 1.7% to 1.5%.

Meanwhile, an earlier report stated that the Chinese central bank will permit funds of which brokers can utilize to purchase stocks as part of numerous measures to stimulate the economy and encourage investor sentiment, in addition to a plan to create particular refinancing for listed companies.

The PBOC will establish a swap facility where securities, fund, and insurance companies can make use of the central bank’s liquidity for the above-stated purpose, said Pan Gongsheng.

Pan also highlighted the potential reduction of the loan prime rate by 0.2 to 0.25 percentage points, without specifying whether it pertains to the one-year or five-year rate. The current one-year LPR stands at 3.35%, and the five-year LPR at 3.85%. Additionally, initiatives were unveiled to support China’s ailing property sector by reducing borrowing costs on up to $5.3 trillion in mortgages and relaxing regulations for second-home purchases, including lowering the down-payment ratio to 15% from 25%.

Following the announcement, the Hang Seng Mainland Properties Index surged by 5% when Hong Kong markets commenced trading. Hong Kong-listed shares of real estate giants such as China Resources Land, Longfor Group Holdings, and China Overseas Land & Investment experienced substantial gains, with increases of up to 2.84%, 3.31%, and 4.22% respectively.

According to a note from Standard Chartered, the Chinese authorities unveiled the most substantial economic support package since at least 2020, encompassing extensive assistance for the real estate market, stock market, corporate lending, and monetary policy easing. These measures are anticipated to expand the PBOC balance sheet, stabilize credit growth, alleviate real estate pressures, provide robust support to the real economy, enhance risk sentiment for China assets, and potentially pave the way for additional stimulus actions in the future.